Q2 2026 Quarterly Investment Report

A Message from the Chief Investment Officer

The second quarter of 2026 was defined by one of the most consequential geopolitical events in recent memory — the US-Iran war and the closure of the Strait of Hormuz — and by the remarkable speed with which markets recovered once a path to resolution emerged. Against a backdrop of surging energy prices, a global bond selloff, and a pivotal leadership transition at the Federal Reserve, equity markets delivered strong returns by quarter-end, rewarding investors who maintained discipline through a volatile mid-quarter period. Fixed income markets were more challenged, and the Canadian dollar weakened as the domestic economy navigated a technical recession.

In the second quarter, our JCIC Balanced Fund gained 7.4%, while the JCIC Equity Fund rose 10.2%. By strategy, the Global Growth Equity portfolio returned 20.4%, the International Equity portfolio returned 12.5%, the US Equity portfolio returned 10.8%, and the Canadian Equity portfolio returned 5.3%. All figures are in Canadian dollars.

The Defining Event: The US-Iran War and the Strait of Hormuz

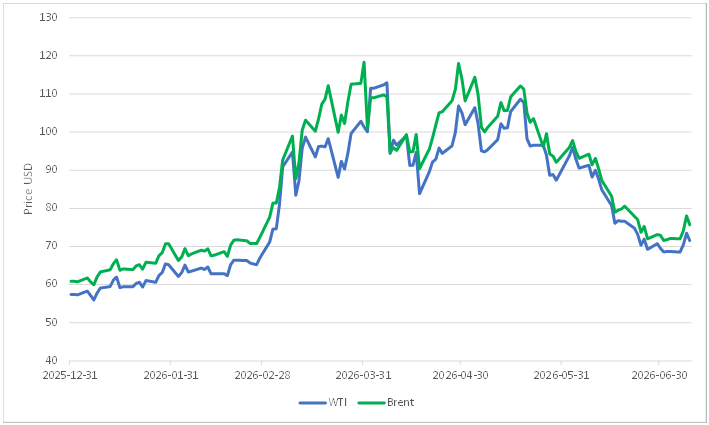

The conflict between the United States and Iran — which began prior to the quarter — cast a long shadow over global markets throughout April, May, and into June. The Strait of Hormuz, through which approximately 20% of the world's seaborne oil transits, remained effectively closed for much of the quarter, triggering a scramble for crude cargoes globally and pushing WTI crude oil above $100/barrel at the start of April (Figure 1).

Figure 1. WTI and Brent oil price per barrel (Source: Bloomberg)

Cyclical uncertainty

A fragile ceasefire reached in April gave way to renewed hostilities in June. The pivotal turning point came on June 14–15, when the US and Iran announced an interim peace agreement to reopen the Strait of Hormuz and begin 60-day negotiations on Iran's nuclear program. The deal was formally signed in Switzerland on approximately June 18–19, and the US declared an end to its naval blockade. The US Treasury simultaneously issued a 60-day license authorizing Iran to sell its oil and energy products, a sweeping reversal of years of sanctions. Ceasefire violations and drone attacks on cargo ships have continued in July to create uncertainty. However, we still believe the direction of travel is still toward de-escalation given President Trump's desire for an off ramp going into US mid-term elections in November.

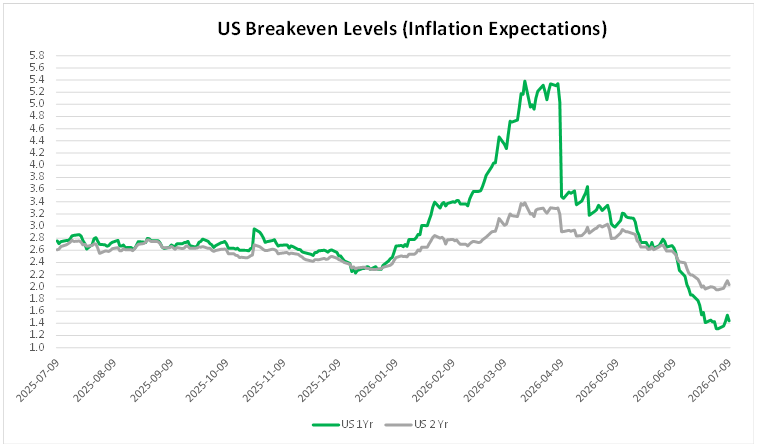

Upon the ceasefire announcement, the market reaction was swift and powerful. Equities surged, bonds rallied, and oil prices collapsed — WTI fell from approximately $100/barrel at the start of the quarter to $69.50/barrel by June 30, a decline of over 30%. This weakness in energy prices has had the effect of reduced inflation expectations in the future. Figure 2 below shows US inflation expectations one and two years from now, which clearly shows significant moderation. However, oil prices have been rebounding in July, following renewed hostilities.

Figure 2. US Breakeven Levels — Inflation Expectations (Source: Bloomberg)

Equity Market Concentration

Despite the turbulence of the middle of the quarter, equity markets delivered strong returns by June 30, driven by the Iran deal, resilient US economic data, and a powerful technology hardware-led rally.

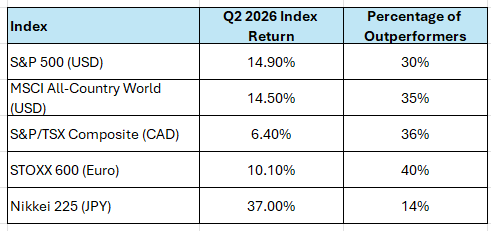

While returns during the quarter were very strong, market breadth was narrow and primarily focussed on AI direct and indirect related earnings potential. Looking at the percentage of stocks outperforming the underlying index in table 1, we can see that almost two thirds of stocks underperformed. Markets with greater breadth (Canada and Europe) also correlate to markets with less exposure to AI beneficiaries but also delivering the weaker market returns. Those companies considered to be potentially disintermediated by AI demonstrated the weakest performance.

We believe the second half of the year will see broader market performance as the singular focus on AI has just reached a level where those companies underperforming from AI fears have de-rated to attractive levels. This does not mean we think AI beneficiaries will not continue to perform. We see AI development a long term secular theme for years to come and can find attractive growth opportunities with reasonable valuation amongst the recent volatility in technology stocks.

Table 1. Equity market breadth (Source: Bloomberg)

Fixed Income Markets

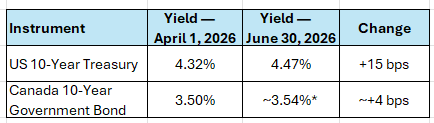

The bond market experienced significant volatility during the quarter. The closure of the Strait of Hormuz drove energy prices sharply higher, stoking inflation fears and triggering a global bond selloff through May. The US 10-year Treasury yield rose from 4.32% at the start of April to a peak of approximately 4.67% in mid-May — with the 30-year yield briefly touching its highest level since 2007 — before partially recovering as the Iran deal took hold. The 10-year yield ended the quarter at 4.47%, approximately 15 basis points higher than where it began.

The Canadian 10-year government bond yield followed a similar trajectory, rising from 3.50% at the start of April to approximately 3.70% in mid-May before easing. Canadian bonds rallied following the Bank of Canada's June decision, as Governor Macklem described the domestic economy as "weak."

Table 2. (Source: Bloomberg)

*Canadian 10-year yield at June 30 is approximate based on available data.

Central Banks

United States — Federal Reserve

The Federal Reserve held its benchmark rate steady at 3.50%–3.75% throughout the quarter, but the policy debate shifted materially. Kevin Warsh assumed the chairmanship in late May, inheriting a central bank facing surging energy-driven inflation and a resilient labor market.

At the June meeting, the FOMC again held rates unchanged, but the updated dot plot showed nine of eighteen officials penciling in at least one rate hike by year-end. Warsh vowed to restore price stability at his debut press conference, though he offered limited forward guidance on the rate path. Currently, markets are pricing a very high probability of a rate hike this fall.

Canada — Bank of Canada

The Bank of Canada held its overnight rate at 2.25% for a fifth consecutive meeting in June, navigating a difficult policy dilemma: a weakening domestic economy on one hand, and war-driven inflation pressures on the other. Canada entered a technical recession after GDP contracted 0.1% annualized in Q1 2026, following a 1.0% contraction in Q4 2025. Economists slashed their 2026 growth forecasts to just 0.7% — the weakest since 2015 outside of the pandemic.

However, early Q2 data offered some encouragement: GDP rose 0.5% in April and 0.1% in May (flash estimate), suggesting a meaningful rebound is underway. The Bank of Canada did not rule out future rate adjustments in either direction, acknowledging that uncertainty remains "unusually elevated." Markets are not pricing in a rate hike this fall but potentially by year end.

Looking Ahead to Q3 2026

As we enter the third quarter, several key risks and opportunities merit close attention:

US-Iran negotiations: The 60-day clock on the interim peace agreement began on approximately June 19. The durability of the ceasefire — and the pace of Iranian oil returning to market — will be the single most important variable for energy prices, inflation, and global growth. Ceasefire violations and drone attacks since late June has resulted in President Trump declaring the cease fire as over on July 8th but negotiations are still ongoing.

Federal Reserve policy: With PCE inflation at 4.1% and a hawkish new chairman, the risk of a rate hike has risen materially. Markets are pricing a meaningful probability of action for this fall. The path of US rates will be a key driver of equity valuations and fixed income returns.

Canadian economic recovery: Early Q2 GDP data suggest Canada's technical recession may be short-lived. The Bank of Canada's next move — cut or hike — will depend heavily on whether energy-driven inflation broadens into the domestic economy.

Technology and AI earnings: The Nasdaq 100's 26% quarterly gain reflects elevated expectations for AI-driven earnings growth. Q3 earnings season will be a critical test of whether those expectations are justified.

Our approach continues to be guided by prudent risk management, rigorous research, and a commitment to preserving and growing capital over time. By remaining selective and investing with conviction, we aim to build resilient portfolios that can navigate changing market conditions while capturing opportunities created by long-term structural trends.

We appreciate the trust you place in us and remain dedicated to helping you achieve your financial objectives. Should you have any questions about your portfolio, our investment strategy, or the broader market environment, we encourage you to reach out. We always welcome the opportunity to discuss your goals and how we are positioning your investments for the future.

Disclosure:

Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter are those of JCIC Asset Management, its editors and contributors, and may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. We strongly advise you to discuss your investment options with your Relationship Manager prior to making any investments, including whether any investment is suitable for your specific needs.

The information provided in our newsletter is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. JCIC Asset Management reserves all rights to the content of this newsletter.

* Performance percentages stated are gross of fees.