First Quarter Performance Report

Geo-Politics, Market Trends, and Opportunities

This report is presented by Kai Lam, JCIC’s Chief Investment Officer.

Top Line Observations

As we close the first quarter of 2026, we are pleased to provide our perspective on the key market developments, economic trends, and investment implications that shaped the period from January through March.

The first quarter of 2026 presented investors with a complex and dynamic environment. This included the United States executing a military strike on Venezuela that captured President Nicolas Maduro, restricting oil shipments to Cuba in order to apply pressure on political change, threats to annex or acquire Greenland, threats to increase tariffs on numerous countries and starting an armed conflict with Iran. There was also volatility surrounding AI spending risks, with funds flowing towards AI-resistant sectors. Despite all of this headline noise and market rotation, ultimately, the JCIC Balanced Fund was down only modestly during the quarter.

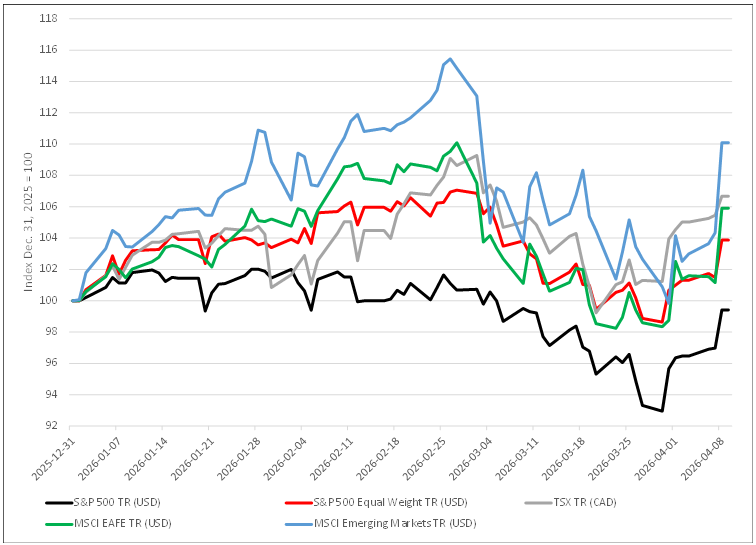

We observed significant rotation across various regions (Figure 1) and across multiple sectors. Canadian and international equities, including emerging markets, began the year strongly but have since moderated amid rising energy prices and the initiation of the Iran conflict. Within U.S. equities, the “Magnificent 7” has notably lagged the broader market, with companies such as Microsoft, Alphabet, Meta, Tesla, NVIDIA, Amazon, and Apple underperforming year to date. In contrast, the equally weighted S&P 500 has outperformed its market-cap-weighted counterpart by over four percentage points.

Figure 1. Year-to-date Indices Total Return

Source: Bloomberg

Artificial Intelligence, Gold, and Oil

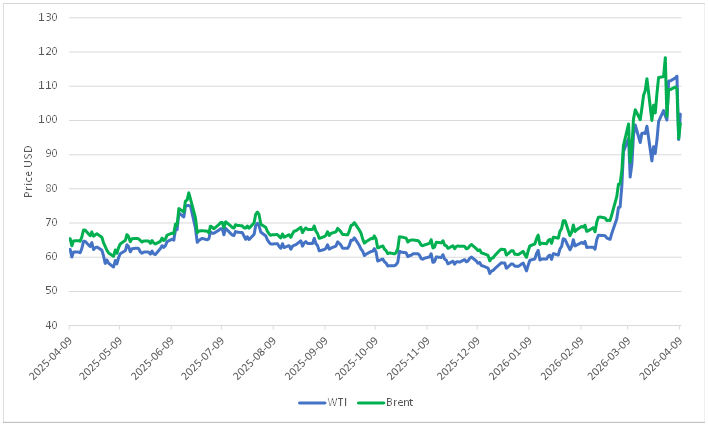

There has also been significant rotation and divergence between subsectors. Concerns about the impact of AI have hurt sentiment across all software companies, and concerns about AI spending plans have impacted the performance of hyperscalers investing in AI. While other sectors, such as staples and utilities, initially performed well as investors sought refuge from poor AI sentiment, those sectors too have moderated since the start of the Iran war as investors sold expensive winners. Even gold, which performed well at first, has underperformed since the start of the war due to elevated valuations and higher real rates (Figure 2), with long bond yields rising faster than inflation expectations, which have also risen due to much higher energy prices. The major winner so far this year has been energy, with the WTI oil price rising from $67/bbl prior to the Iran war to peak at $113 (Figure 3).

Figure 2. US Real Rates (US 10 Year Treasury Inflation Protected Securities Yield)

Source: Bloomberg

Figure 3. Oil Price USD/bbl

Source: Bloomberg

Underlying Market Strength

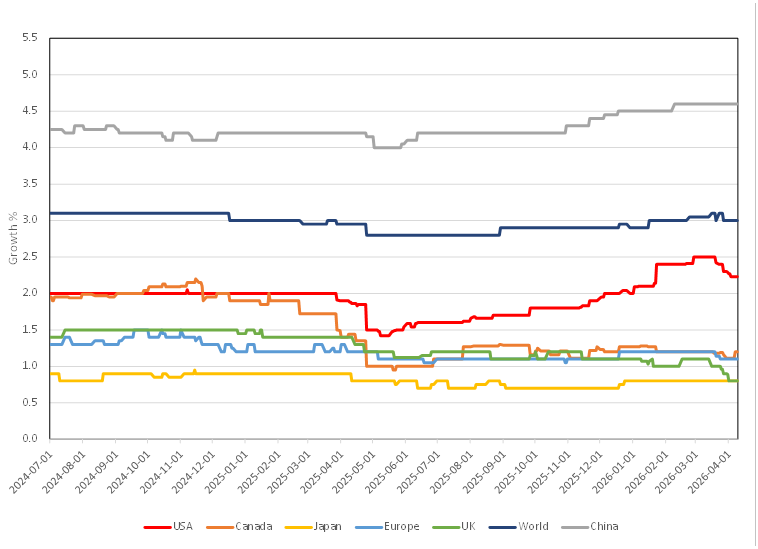

Given the magnitude of geopolitical risks and inflationary pressures, a key question is why markets have not declined more significantly. While higher energy prices have led to modest downward revisions in 2026 global GDP forecasts (Figure 4), these adjustments have been relatively contained. Importantly, much of the current uncertainty is policy-driven and therefore potentially reversible.

Figure 4. 2026 GDP Growth (%) Forecast

Source: Bloomberg

The Price of Oil Futures

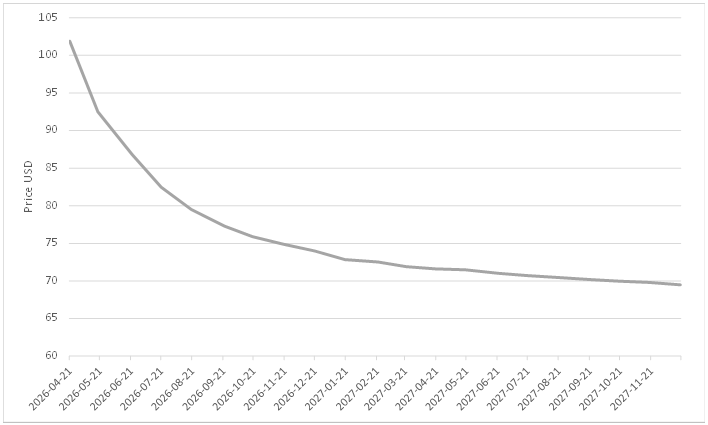

This view is reflected in the oil futures curve (Figure 5), which suggests that markets are anticipating a de-escalation of the Iran conflict. Futures prices imply a gradual normalization in oil prices, albeit at levels somewhat above pre-conflict conditions, reflecting the time required to restore supply capacity and normalize transportation flows.

While the timing of any de-escalation remains uncertain, there are political incentives for resolution. The conflict has proven unpopular domestically. With U.S. midterm elections approaching, the administration faces increasing pressure, as election outcomes could significantly impact legislative control and the ability to advance policy objectives. These dynamics may encourage a sooner-than-expected resolution.

Figure 5. WTI Futures Contract Price USD/bbl

Source: Bloomberg

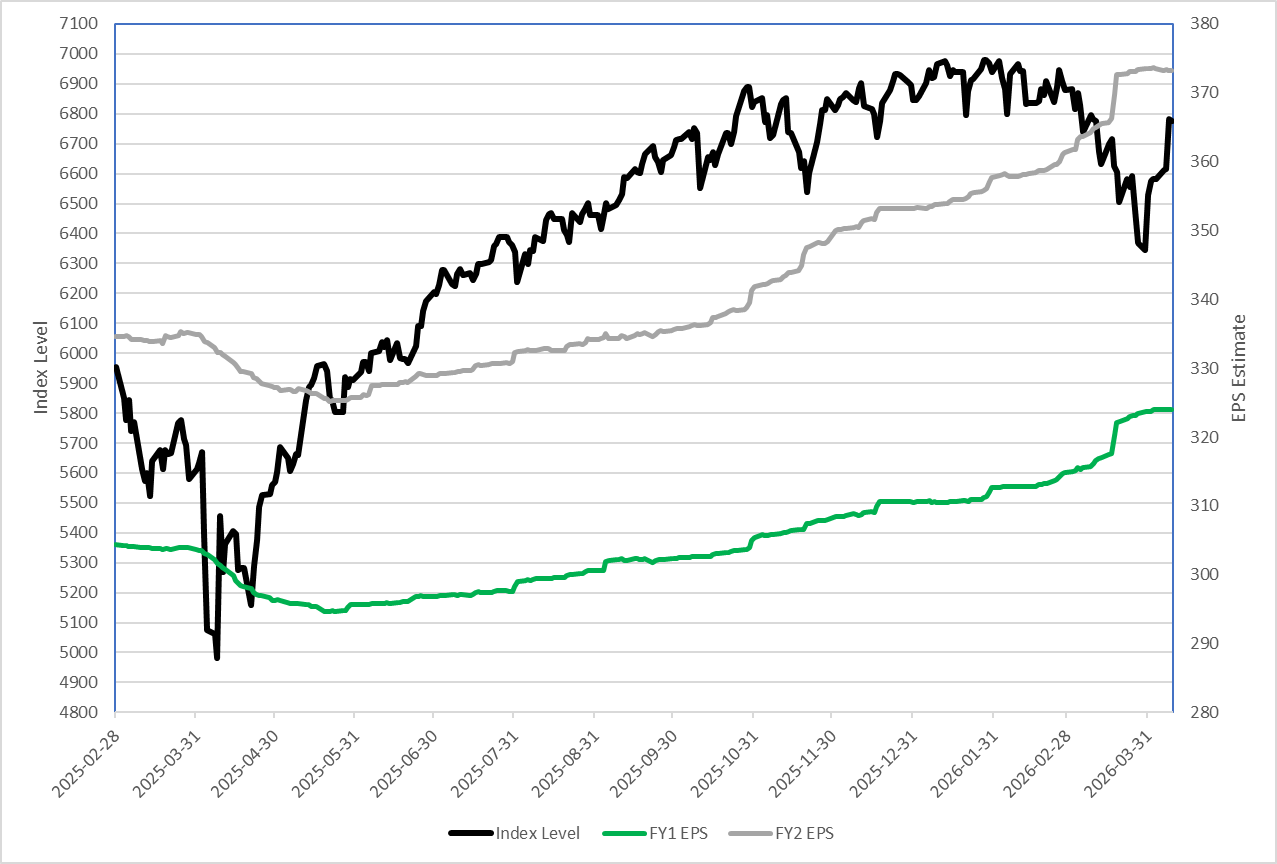

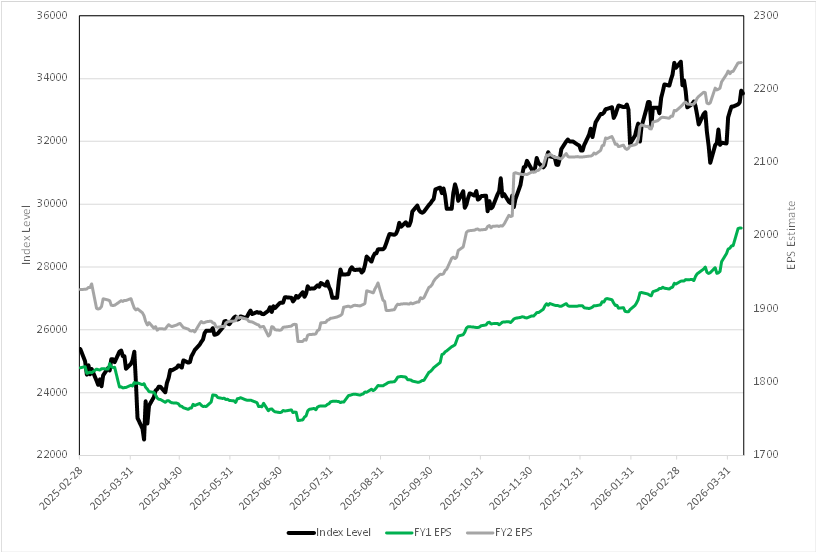

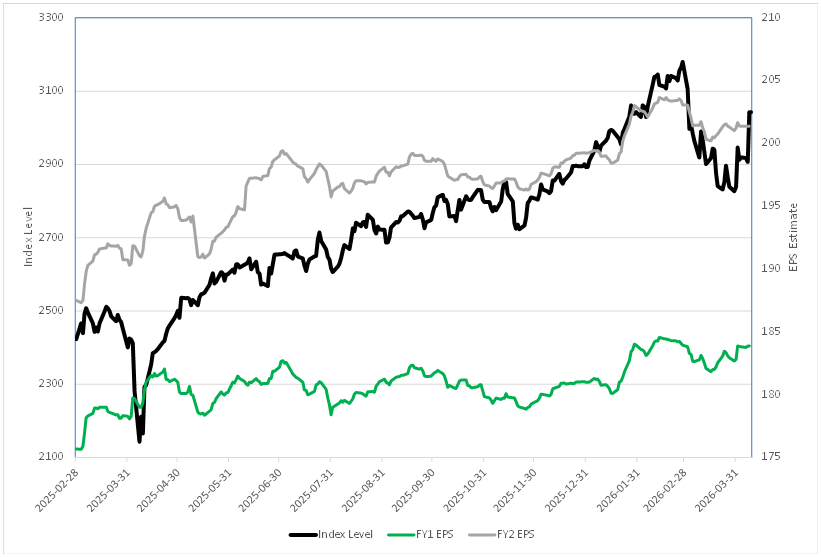

Strong Earnings Performance

Beyond geopolitics, earnings expectations remain constructive. Consensus estimates continue to project solid growth in 2026, with double-digit earnings growth anticipated in the U.S. and Canada, and high single-digit growth in international developed markets (Figures 6–8). Artificial intelligence remains a key driver, contributing through both capital investment and productivity gains as companies integrate AI into their operations.

Figure 6. S&P 500 EPS Estimates vs. Index

Source: Bloomberg

Figure 7. TSX EPS Estimates vs. Index

Source: Bloomberg

Figure 8. MSCI EAFE EPS Estimates vs. Index

Source: Bloomberg

Where We Are Looking for Growth

The quarter’s significant market rotation has created opportunities to selectively increase exposure to attractive areas.

In fixed income, rising bond yields—driven in part by higher energy prices—have pressured prices and improved forward return potential. This allowed us to reduce our underweight position in fixed income and deploy a portion of our elevated cash holdings.

In equities, we capitalized on corrections in sectors such as technology, metals and mining, and financials, where valuations became more compelling.

While we have remained tactically responsive to evolving market conditions, our core investment approach continues to emphasize high-quality companies with strong earnings potential, robust cash flow generation, solid balance sheets, and experienced management teams.

The Next Nine Months

The investment landscape for the remainder of 2026 will likely be shaped by the interplay between geopolitical events, economic performance, inflation persistence, and policy responses. We anticipate continued volatility and believe that active management, disciplined risk management, and a long-term perspective will be essential to successfully navigating the environment.

Key catalysts to monitor in the coming quarters include:

· Federal Reserve policy decisions and communication regarding the rate path

· Corporate earnings trends and management guidance

· Geopolitical developments and their economic implications

· Evolution of AI adoption and its impact on productivity and profitability

In Summary

While the first quarter presented challenges, it also reinforced the importance of maintaining a disciplined investment approach. Markets have historically rewarded patient, long-term investors who remain focused on fundamentals rather than short-term noise.

We remain committed to stewarding your capital with the care and diligence it deserves. Our investment philosophy emphasizes preservation of capital, thoughtful risk-taking, and positioning portfolios to benefit from long-term secular trends while managing downside risks.

As always, we welcome the opportunity to discuss your specific circumstances, goals, and any questions you may have about your portfolio or our market outlook.

Thank you for your continued trust and confidence.

If you have questions about any of this information, please don’t hesitate to reach out to us:

Disclosure:

Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter are those of JCIC Asset Management, its editors and contributors, and may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. We strongly advise you to discuss your investment options with your Relationship Manager prior to making any investments, including whether any investment is suitable for your specific needs.

The information provided in our newsletter is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. JCIC Asset Management reserves all rights to the content of this newsletter.

* Performance percentages stated are gross of fees.