Signs Hint That a Broader U.S. Stock Market Rally May Be Taking Hold

U.S. stock bulls have successfully fueled a market rally this year, persisting despite bouts of volatility, mixed economic data, and a fraught outlook for interest rates.

The S&P 500 entered a new bull market after rising more than 20% from the humbling lows experienced last fall—capping the longest bear market since 1948, according to Dow Jones data. Year to date, this broad measure of U.S. stocks is up over 10%.

A growing multitude of sectors, spanning from small caps to select energy names, are beginning to exhibit encouraging indicators that this market resilience is finally broadening below the surface.

Portfolio Positioning: Our U.S. Exposure

We closely monitor and scrutinize the trajectory of U.S. markets daily to determine how best to allocate our clients’ money. Our current target asset allocations reflect a grounded conviction in U.S. equities:

| JCIC Portfolio | U.S. Stock Weighting |

|---|---|

| Balanced Portfolio | 28% |

| Growth Portfolio | 36% |

| Equity Portfolio | 44% |

Despite ongoing concerns surrounding interest rates and recession risks, under-the-surface data suggests this U.S. rally has sustainable legs

Signs of Momentum and Expanding Market Breadth

To start, investor sentiment has been steadily rising according to polling from the American Association of Individual Investors (AAII). Concurrently, data tracking both retail and institutional fund flows indicates that money previously sitting on the sidelines for much of the year is actively moving back into equities.

Perhaps the most encouraging development is the rally’s expanding "market breadth"—the total number of individual stocks participating in the upward move. We are finally seeing a lift in shares well beyond the mega-cap technology giants that single-handedly led the index higher earlier in the year.

Russell 2000, March 18-June 28, 2023

Source: JCIC Asset Management Inc.

The Small-Cap Resurgence

The Russell 2000, which tracks 2,000 of the smallest publicly traded companies in the United States, rallied 5% through June. While the Russell index remains roughly 25% below its 2021 all-time high on a percentage basis, this sudden shift in momentum is excellent news for broader market health.

More broadly, the climb of small caps indicates that investors are becoming more constructive about the macroeconomic outlook. It serves as a clear signal that the foundational health of the world’s largest economy is stronger than consensus realizations suggest.

US Commercial Bank Deposits

Source: Bloomberg

The Consumer Resilience Factor: Cash on Hand

Our constructive view is heavily informed by a metric we continue to track closely within U.S. households: spendable cash reserves. This is a point we have stressed in recent months, and it bears repeating—consumers still possess a significant cushion of excess savings in the bank. This extra cash explains why households have remained uniquely resilient in absorbing ongoing inflation pressures.

U.S. commercial bank deposits experienced a historic spike in March 2020 at the onset of COVID-19 restrictions. While this massive savings glut has peaked and is steadily drawing down, it has not yet fully reverted back to its long-term historical trend line. There is still meaningful liquidity left to be spent.

This persistent pool of consumer cash directly explains recent upward movements in the consumer discretionary space, where hard-hit sub-sectors like cruise lines and hotel operators are beginning to participate in the market’s rise.

Signs Of a Broadening Rally

Source: Bloomberg

Energy Stabilizes and Earnings Expectations Reset

Another classic indication of a durable market rally is the quiet firming up of the energy complex. Oil and gas companies have largely lagged through the first half of 2023, following a stellar outperformance in 2022. However, in recent weeks, several large-cap U.S. integrated producers have seen their valuations steadily turn upward.

While "mega-caps" like Amazon and Apple remain the clear market leaders, the rally that began with them is cleanly broadening out. This is evidenced by the upward trajectory of both the Russell 2000 and the equal-weighted S&P 500 index—which strips away the distorting effects of market-cap weightings to prove that a rising tide is lifting a wider array of companies.

Source: Bloomberg

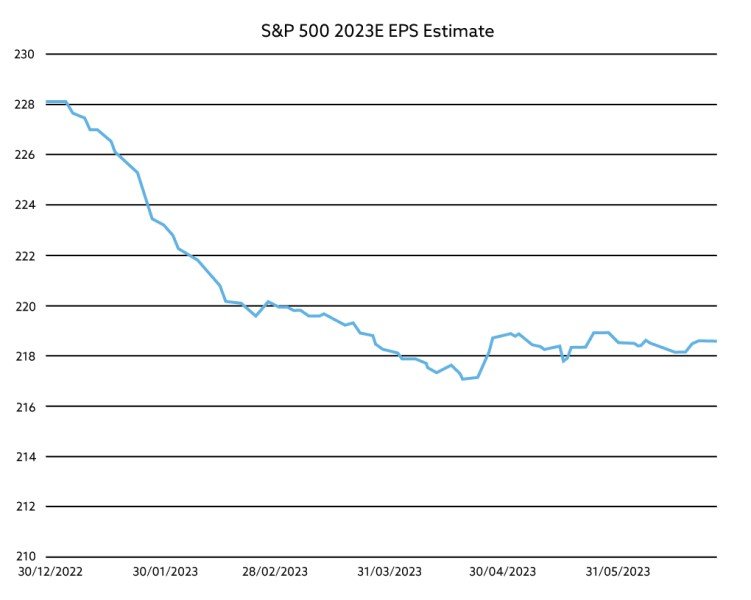

Realism Returns to Corporate Earnings

Corporate earnings expectations have also normalized constructively. Throughout last year, consensus estimates for 2023 earnings per share (EPS) were overtly optimistic and inconsistent with slowing economic data.

Over the past few months, those estimates have come down to realistic, stabilized levels. This reset creates a much sturdier fundamental foundation that is supportive of recent equity performance.

The Outlook for the Second Half of 2023

This data does not guarantee that the remainder of 2023 will be a smooth, unbroken bull market. Much like global central banks, our investment decisions remain entirely data-dependent. Major institutional strategists, including JP Morgan, suggest that the third and fourth quarters will be choppy as the Federal Reserve keeps interest rates elevated to combat sticky core inflation.

Investors should expect further bouts of volatility, and the interest rate environment will undoubtedly remain fraught. However, looking at the expanding breadth of participating sectors, market bulls currently appear to have more room to run.

Partner with JCIC

As your portfolio managers, our primary goal is to make the complexities of investing simple and transparent for you. Whether you have questions about your asset allocation, need tactical assistance, or simply want to discuss shifting market trends, please feel free to reach out to us at any time. We are always here to guide your investment journey.

Disclosure: Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter are those of JCIC Asset Management, its editors and contributors, and may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it.

The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable.

We strongly advise you to discuss your investment options with your Relationship Manager prior to making any investments, including whether any investment is suitable for your specific needs.

The information provided in our newsletter is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. JCIC Asset Management reserves all rights to the content of this newsletter.